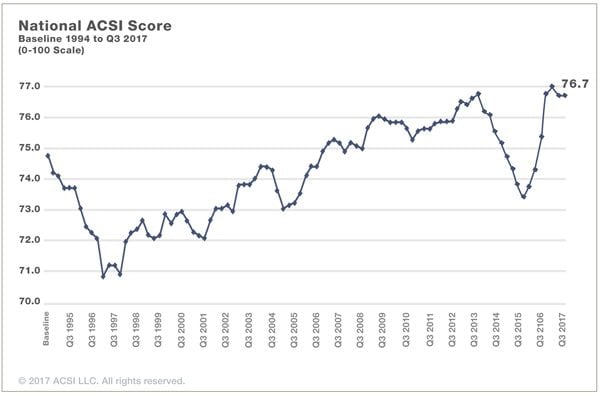

ANN ARBOR, Mich. (December 12, 2017) — The national level of customer satisfaction stabilizes in the third quarter, according to the American Customer Satisfaction Index (ACSI®). Overall U.S. customer satisfaction is steady at an ACSI score of 76.7 (on a 0-100 scale) following recent periods of both sustained decline and improvement.

While customer satisfaction grew consistently throughout 2016, this year has been volatile, with ACSI up in the first quarter, down in the second, and now flat in the third. For a long period after the Great Recession, consumer spending growth was positive but weak, and so was ACSI growth. By the end of 2013, consumer spending rebounded strongly, causing service and quality glitches and a decline in customer satisfaction. But the pent-up demand was so strong that a decline in customer satisfaction had little impact on demand. As the pace of spending growth slowed, customer satisfaction recovered.

For the U.S. economy to be strong, consumer spending – which accounts for two-thirds of the GDP – needs to be strong as well. Greater customer satisfaction last year did not translate to rapid contemporaneous economic growth, but seems to be paying dividends for the economy this year. GDP growth topped the 3.0 percent mark in both the second and third quarters of 2017 – a first since the middle of 2014.

The growth in consumer spending, however, is still not robust enough to sustain the kind of GDP growth needed to make the recently passed tax plan revenue neutral. Further, much of the increase in consumer spending has been financed by debt. As it surpassed 13 trillion dollars, household debt is now higher than it was in 2009.

In large measure, household willingness to take on more debt for consumption is due to low wage growth coupled with high customer satisfaction and confidence. Yet, the economy is more solid than it was before the recession, with lower debt as a share of economic output. Nevertheless, demand is still not strong enough to propel much more GDP growth.

What’s needed are additional household discretionary income and continued high levels of both customer satisfaction and confidence. Employment is about as robust as it can be, but without better wage growth, there is a risk of even more household debt and subsequent delinquencies, especially since a fair number of the loans are subprime.

This press release is also available in PDF format.